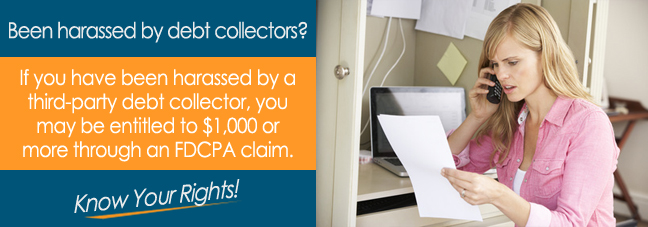

Are debt collectors waking you up in the middle of the night with rude and belligerent demands? Are your friends and family being told about your debt? Collection agencies often use these tactics to intimidate or alarm consumers into paying, but such actions are illegal. Read on to learn more about your rights.

Your Rights Under the FDCPA

The Fair Debt Collection Practices Act, or FDCPA, is a law that regulates the professional conduct of third-party debt collectors. If you owe a debt and a collection agency uses any of the strategies below to stress you into paying, you can sue.

- Raising their voice and making threats

- Contacting you even after you’ve ordered them to cease communications

- Calling you at inconvenient times and places, such as before 8:00 a.m. and after 9:00 p.m. in your time zone

- Swearing and using profane language

- Refusal to provide you with information about the debt

- Demanding amounts that exceed the original debt

Need Help With Reviver Financial?

Call for a Free Case Evaluation Now!

Company Profile: Reviver Financial, LLC

If you are being called by Reviver Financial, LLC, we have collected a company overview and posted it below.

Reviver Financial, LLC, which also does business as Security One Lending, is a debt collection agency in Hutchinson, Kansas. It was founded in 2013, has 116 employees, and is managed by Bradley E. Hochstein.

Litigation information archived at the PACER website confirms that people who thought they were being harassed by Reviver Financial, LLC refused to pay.

![Are You Being Called By Reviver Financial, LLC?*]()

Need Help With Reviver Financial?

Call for a Free Case Evaluation Now!

Alleged Violations against Reviver Financial, LLC

According to PACER, on or about June 14, 2016, Reviver Financial, LLC used an agent to send a collection letter to a Wisconsin consumer. The debt in question was a payday loan, and the letter made representations that the collector held a Wisconsin Collection Agency License.

When the consumer’s attorney contacted the Division of Banking, they confirmed that the company did not hold a Wisconsin collection agency license.

Feeling harassed by Reviver Financial, LLC, the consumer filed an FDCPA lawsuit against the company for allegedly:

- Claiming to hold a collection agency license when it didn’t

- Using false, deceptive, and misleading means to collect a debt

The matter was later dismissed.

Need Help With Reviver Financial?

Call for a Free Case Evaluation Now!

Hire an Attorney

The phone number for this debt collection agency is 1-888-768-0674. If you ever see it calling your phone, it means that a debt collector is trying to reach you. If they claim to be licensed to collect debts in your state but an investigation proves otherwise, hire a consumer lawyer and file a claim against Reviver Financial, LLC. If you win your case, you could be awarded $1,000 per FDCPA violation in addition to other damages, so when a collection agency disregards your rights, don’t be afraid to fight back.

Need Help With Reviver Financial?

Call for a Free Case Evaluation Now!

Additional Resources

Case taken from PACER (pacer.gov). File number is Case 2:17-cv-00816-DEJ from the United States District Court for the Eastern District of Wisconsin, Milwaukee Division.

*Disclaimer: The content of this article serves only to provide information and should not be constructed as legal advice. If you file a claim against Reviver Financial, LLC or any other third-party collection agency, you may not be entitled to any compensation.