You don’t have to take the abuse and harassment dished out by a debt collection agency. A large majority of consumers don’t know they enjoy numerous rights granted by a federal consumer protection law.

In the late 1960s and early 1970s, a rapidly growing number of consumers told political leaders they were fed up with aggressive third party debt collector tactics.

After several years of back and forth between American citizens and the United States Congress, the landmark Fair Debt Collection Practices Act (FDCPA) became law.

The FDCPA clearly lists illegal debt collection practices, as well as provides consumers with a legal remedy that allows them to seek compensation for suffering from bill collector induced physical and emotional distress.

How Maryland Deals with Aggressive Debt Collection Agencies

Congress passed the FDCPA to create a comprehensive consumer protection law that would cover every American. Politicians from both parties encouraged states to draft their own versions of the FDCPA and within five years after the enactment of the federal FDCPA, many states followed suit with the passage of FDCPA laws.

Maryland has been considered one of the leaders in the movement to handcuff third party debt collectors. Although Maryland FDCPA laws are similar to what is written into the federal FDCPA, Maryland offers additional legal protections for consumers.

For example, Maryland FDCPA laws covers bill collectors and original creditors. The Old Line State also requires debt collection agencies to receive a license for collecting outstanding consumer debts.

![How Maryland's FDCPA Laws Can Help Protect You]()

FDCPA and Maryland Collection Law Protections

One of the legal foundations of the federal FDCPA was to address the aggressive debt collection practice of frequently calling consumers. If a bill collector repeatedly calls you at home or on your cell phone, you have the right under the FDCPA to request the phone calls to stop.

Many debt collection agencies ignore consumer requests and if that happens to you, the FDCPA allows you to work with a FDCPA lawyer to seek monetary damages. The FDCPA also prohibits third party debt collectors from contacting consumers between the hours of 9 pm and 8 am.

Phone calls at work from a bill collector are forbidden, if your employer prohibits such phone calls in the workplace.

Many of the provisions written into Maryland FDCPA laws address the issue of threats. Under Maryland FDCPA laws, a bill collector isn’t allowed to threaten to use force or violence in an attempt to intimidate you into paying off a delinquent debt.

A debt collection agency cannot threaten to seize your property and threaten to disclose personal financial information that would damage your reputation. Maryland FDCPA laws don’t tolerate abusive language and the practice used by bill collectors of communicating with friends and relatives.

The statute of limitations in Maryland for collecting outstanding open accounts such as credit card accounts is three years.

Don’t permit a third party debt collector to intimate you. Speak with a Maryland licensed consumer protection attorney today to learn more about how the FDCPA can help protect you.

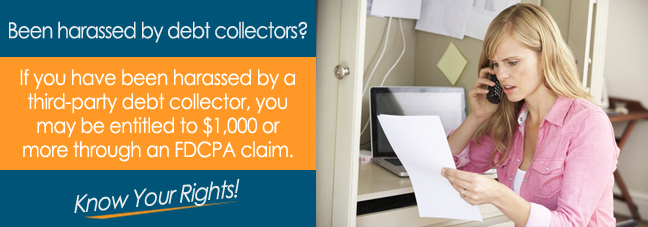

If you believe that a debt collector is violating Maryland’s FDCPA laws, you should seek the help of an FDCPA attorney. You may be able to seek up to $1,000 in damages for each violation of the FDCPA. An attorney will be able to help navigate you through the entire process.

Additional Resources