Receiving a letter from a debt collection agency doesn’t seem like a big deal. After all, you can file the letter in the same way that you file other letters sent by creditors and third party debt collectors: into the trash can.

Although the letters don’t spark much concern, the laid back approach you take for handling an outstanding credit card or personal loan account can morph into acute fear and anxiety the instant a bill collector calls you at work and/or at home. Welcome to debt collections 101.

Before September 20, 1977, consumers had little, if any legal recourse to fight back against the persistent and aggressive tactics implemented by bill collectors.

That has all changed because of the enactment of the landmark Fair Debt Collection Practices Act (FDCPA).

Delaware and the FDCPA

The United States Congress passed the FDCPA into law to ensure every consumer was granted legal protections against aggressive debt collection practices.

Not only does the FDCPA clearly outlaw several debt collection tactics, the groundbreaking federal consumer protection law also allows consumers to sue debt collection agencies for monetary damages.

Suing for financial compensation is highly recommended for consumers that suffer from physical and/or emotional distress.

In addition to the federal FDCPA, every state has passed its version of the consumer protection law.

Although many of the state FDCPA laws close loopholes in the original federal law, Delaware FDCPA laws don’t have the same legal muscle as the strength of the FDCPA laws enacted in states such as California and New York.

In fact, Delaware FDCPA laws were not written to punish bill collectors. Because of friendly tax laws, Delaware is a popular state for businesses to incorporate.

Many credit card corporations received incorporation papers in Delaware, which explains why the state’s FDCPA laws lack legal muscle.

![How Delaware's FDCPA Laws Can Help Protect You]()

Protections Granted by the FDCPA

Your best bet to receive legal protections against debt collection agency harassment is by hiring a consumer protection attorney that thoroughly understands the FDCPA. Under the FDCPA, a third party debt collector cannot call you between 9 pm and 8 am.

Any phone calls received outside of the FDCPA time constraints should prompt you to contact a FDCPA lawyer.

A bill collector is prohibited from taking money out of your bank account, without first following the state’s guidelines for garnishing wages.

You don’t have to put up with debt collection agency threats, which can includes a threat to arrest you for not paying off a delinquent credit card or personal loan balance.

Delaware’s contribution to FDCPA laws comes in the form of the state being a one party consent state.

This means only one person involved in a phone conversation needs to give permission to record the phone call. Delaware also has established a six years statute of limitations on the collection of outstanding consumer debts.

Speak with a Delaware licensed consumer protection lawyer to learn more about how the FDCPA helps protect you.

If you believe that a debt collector is violating Delaware FDCPA laws, you should seek the help of an FDCPA attorney.

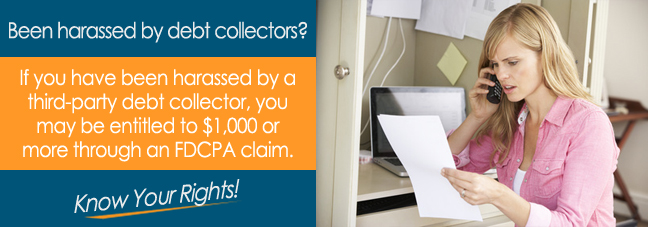

You may be able to seek up to $1,000 in damages for each violation of the FDCPA. An attorney will be able to help navigate you through the entire process.

Additional Resources