After a long meeting at work, you return to your office to soak in what transpired during the meeting. You play back the messages left on the office answering machine and one message gives you considerable concern. A debt collection agency has left a message that you must take care of a consumer debt within a certain period. You think about the alleged debt for a few minutes, and then you decide that the third party debt collector has crossed the legal line by trying to collect a debt you already have paid off.

Deception is a common tactic used by bill collectors that are highly motivated by earning considerable profits. However, a historically significant federal consumer protection law prevents debt collection agencies such as Donald R. Conrad, PLC from implementing deceptive debt collection practices.

About Donald R. Conrad, PLC

As a law firm located in Livonia, Michigan, Donald R. Conrad, PLC represents original creditors in the credit card industry, as well as businesses that handle home and commercial mortgages. The debt collection agency has received a few complaints over the past three years from consumers that have contributed to the Better Business Bureau (BBB) website. With nearly 20 years in business, Donald R. Conrad, PLC has received an A- rating from the BBB, while not gaining enough favorable traction to receive accreditation from the leading consumer advocacy organization.

What Constitutes Misrepresentation

For decades leading up to September of 1977, consumers had little, if any legal recourse in the fight against bill collectors. On September 20, 1977, the United States Congress wrote the Fair Debt Collection Practices Act (FDCPA) into federal law. The landmark federal consumer protection law makes a long list of previously acceptable debt collection techniques illegal. For example, a representative from Donald R. Conrad, PLC cannot call you between the hours of 9 pm and 8am.

The FDCPA also bans the longstanding practice of using deception to trick consumers into paying off outstanding credit card and personal loan balances. Donald R. Conrad, PLC is barred from attempting to collect on a consumer debt that you have already paid off. The law firm also cannot demand that you send more money than you actually owe on a credit card or a personal loan account. As a law firm, Donald R. Conrad, PLC does not violate the FDCPA by claiming to be a law firm. However, most debt collection agencies are not law firms and the companies cannot claim to represent a law firm.

![Did Donald R. Conrad Misrepresent Themselves?*]()

Monetary Damages and the FDCPA

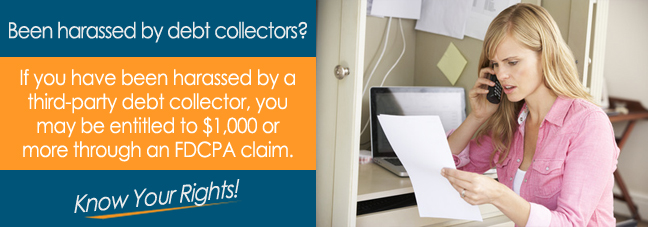

The FDCPA punishes lawbreaking third party debt collectors by giving consumers the power to file a claim seeking statutory damages. With a maximum award of $1,000 statutory damages represent a one-time financial award for every violation of the FDCPA. This means you cannot seek statutory damages against Donald R. Conrad, PLC for one violation of the FDCPA, and then turn around a week later and file a claim seeking a second award for statutory damages.

Fight back against Donald R. Conrad, PLC. Schedule a free initial consultation with a licensed consumer protection lawyer who has considerable experience winning FDCPA cases.

Additional Resources

*Disclaimer: The content of this article serves only to provide information and should not be construed as legal advice. If you file a claim against Donald R. Conrad, PLC, or any other third-party collection agency, you may not be entitled to compensation.