If you took a time machine back to before 1977, you would find a world where debt collection agencies ruled the day. From threatening to seize private property to calling consumers well into the night, third party debt collectors had no legal guidance at the state and federal levels when it came to legislating debt collection efforts. That all changed on September 20, 1977, when the United States Congress passed the most important consumer protection law ever.

Referred to the consumer Bill of Rights, the Fair Debt Collection Practices Act (FDCPA) prohibits a long list of overly aggressive debt collection tactics. Under the FDCPA, a bill collector is not allowed to threaten you in any way. The landmark consumer protection law also prevents debt collection agencies from misrepresenting themselves. Did Scott & Associates misrepresent themselves? If so, you should consider legal action that includes filing a claim against the third party debt collector.

About Scott & Associates

Accredited by the Better Business Bureau (BBB) since 2010, Scott & Associates has received about 20 complaints over the past three years that the leading consumer advocacy organization resolved. Scott & Associates is not a traditional debt collection agency, but instead, it is a law firm responsible for collecting money past due on bank accounts. The law firm has received the highest BBB rating of A+. Scott & Associates opened its door for clients in 2000.

Defining Misrepresentation under the FDCPA

The FDCPA does not just say it is unlawful for third party debt collectors to misrepresent themselves. Under the FDCPA, bill collectors are put on notice to not conduct specific acts of misrepresentation. The FDCPA forbids debt collection agencies from impersonating other organizations, such as law enforcement and government agencies. Sweeping legal language written into the FDCPA bans the once accepted practice of third party debt collectors lying about how much consumers owed on outstanding credit card and personal loan accounts. In addition, a bill collector such as Scott & Associates is not allowed to try to collect more money on a consumer debt than you actually owe.

Seeking Just Compensation for FDCPA Violations

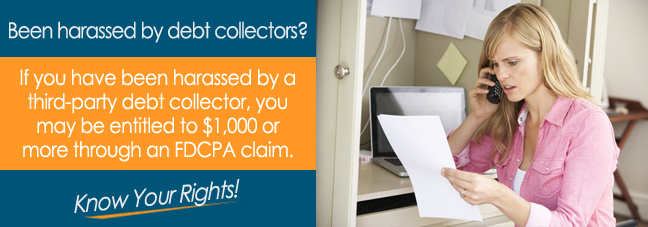

Federal legislators did much more than outlaw certain debt collection tactics. They also added a provision within the FDCPA that grants consumers the right to file claims seeking just compensation for one or more violations of the federal consumer protection law. As the standard type of just compensation for FDCPA cases, statutory damages cover every violation committed by a bill collector. With a maximum reward of $1,000, statutory damages require you to present evidence that proves Scott & Associates violated one or more provisions of the FDCPA. You can also seek financial relief to pay attorney fees, as well as ask for injunctive relief that forces Scott & Associates to stop contacting you.

![Did Scott & Associates Misrepresent Themselves?*]()

Work with a Licensed FDCPA Lawyer

All of the legal protections provided by the FDCPA mean nothing, unless you work with a licensed consumer protection attorney. Your FDCPA lawyer will present the evidence required to move your claim forward in a civil court. Schedule a free initial consultation with an FDCPA lawyer today to get the ball rolling on your case.

Additional Reading

*Disclaimer: The content of this article serves only to provide information and should not be construed as legal advice. If you file a claim against Scott & Associates, or any other third-party collection agency, you may not be entitled to compensation.