With high profit margins acting as motivation, far too many debt collection agencies violate a landmark consumer protection law by harassing and intimidating consumers into paying off outstanding credit card and personal loan accounts. Harassment and intimidation can involve tactics such as making forceful phone calls at all hours of the day. Although overly aggressive debt collection tactics receive most of the attention, a Landmark federal consumer protection law also prohibits third party debt collection from using deception to trick consumers into paying off delinquent debts.

Passed by the United State Congress on September 20, 1977, the Fair Debt Collection Practices Act (FDCPA) clearly makes it illegal for bill collectors to issue of threats of any kind. The consumer protection law outlaws physical threats, as well as threats to confiscate private property for liquidation into cash. In addition, the FDCPA forbids debt collection agencies from making false statements regarding consumer debts.

What Exactly are False Statements?

The United States Congress did much more than simply write a generic law that states it is unlawful for third party debt collectors to harass and intimidate consumers. According to the false statement provision of the FDCPA, a bill collector such as Pressler & Pressler cannot impersonate another organization in an attempt to trick you into taking care of an outstanding credit card or personal loan balance. Impersonating the IRS is an especially bold and illegal form of deception. Some companies impersonate the IRS to leverage the tax collecting organization’s intimidating reputation. Debt collection agencies also break the law when they impersonate a law enforcement agency.

False Statements Must be “Material”

Although there is not any reference within the FDCPA, any false statement made by a third party debt collector must be material to the case. Rulings subsequent to the enactment of the FDCPA have created the “material” standard for proving allegations of false statements. Material means that a false statement made by a bill collector like Pressler & Pressler had a direct impact on how you reached one or more financial decisions.

For example, a debt collection agency might have claimed you owe more than you actually owe on a credit card account. The false statement might have motivated you to move money around a couple of your personal banking accounts to prevent the company from issuing a garnishment order. Under the FDCPA, this type of false statement is considered a material factor in how you reached a personal finance decision.

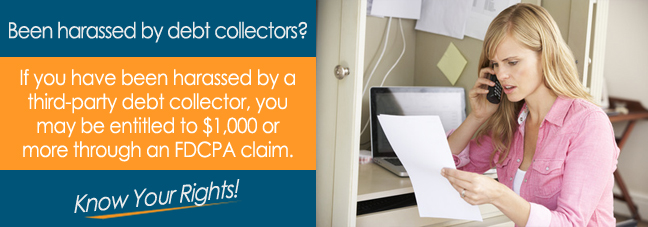

Possible Money Damages

The FDCPA does much more than make a long list of previously acceptable debt collection actions illegal. You also have the right to sue an unlawful company for violating one or more provisions of the federal consumer protection law. As the most basic type of monetary award, statutory damages cover every violation of the FDCPA committed by the same company. Lawmakers capped statutory damages at $1,000, which means you have to sue for actual damages in a case the involves physical and/or emotional distress symptoms.

![Did Pressler & Pressler Make False Statement Regarding Debt?]()

Speak with a Licensed FDCPA Attorney

Claiming Pressler & Pressler made one or more false statements is a serious charge. The debt collection agency will respond by working with a team of seasoned lawyers. You cannot expect to win an FDCPA claim, unless you balance the scales of justice by hiring an experienced FDCPA attorney. Most consumer protection lawyers schedule free initial consultations with clients to determine the best course of legal action.

Additional Resource

*Disclaimer: The content of this article serves only to provide information and should not be construed as legal advice. If you file a claim against Pressler & Pressler, or any other third-party collection agency, you may not be entitled to compensation.