If you have fallen behind on keeping up with your personal financial obligations, then you understand the pressure faced by millions of Americans that have fallen into a deep financial hole. Pressure quickly turns into incredible stress, when a debt collection agency such as Covington Credit begins to harass you at home and at work.

Fortunately, a long standing federal consumer protection law protects consumers against overly aggressive third party debt collectors.

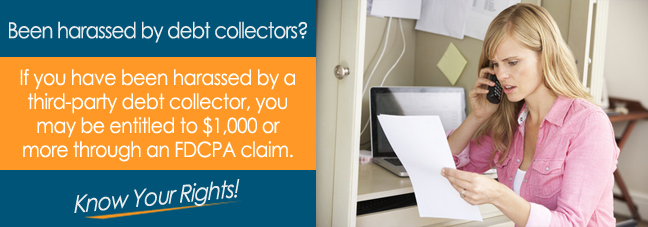

Enacted by the United States Congress on September 20, 1977, the Fair Debt Collection Practices Act (FDCPA) makes it illegal for bill collectors to harass and intimidate consumers. For example, a bill collector is forbidden from threatening you in any way.

The FDCPA also requires debt collection agencies to send a debt validation letter to consumers within a specified period.

Ask for a Debt Validation Letter

Under the FDCPA, third party debt collectors have five days after the first contact with you to send a debt validation letter. Some bill collectors ignore this FDCPA provision, which means you need to request the debt collection agency to send you a debt validation letter to your home address.

A debt validation letter represents the most powerful tool you have to ensure all the information associated with your debt is correct. You can review the letter to confirm the amount owed is right, as well as learn the name of the original creditor.

Responding to a Debt Validation Letter

After receiving a debt validation letter, you should respond promptly to the letter by sending a return debt validation letter. In your version of the debt validation letter, you want to ask for documentation that proves you owe money to the original creditor named in the debt validation letter sent by the bill collector.

The copy of the original contract with the creditor is the type of documentation you should request. You should also ask the debt collection agency to send evidence of when the outstanding debt was established, which typically falls on the day of the last activity on the account.

Knowing the age of the debt helps you establish a timeline to invoke the statute of limitations imposed by your state for debt collection efforts.

![Did Covington Credit Not Validate Your Debt?]()

The Right to Seek Monetary Damages

According to the FDCPA, consumers have the right to seek monetary damages for the pain and suffering caused by illegal debt collection practices. Statutory damages, which the FDCPA limits to $1,000, covers all the FDCPA violations committed by the same company.

Actual damages are associated with the pain and suffering caused by physical and/or emotional duress symptoms. You might suffer from sleepless nights because of worrying about how you will pay off a consumer debt. Lack of sleep can trigger emotional distress symptoms that include mood swings and sudden aggressive outbursts.

Work with an Experienced FDCPA Attorney

Ensuring you benefit from every right written into the FDCPA involves collaborating with a highly rated consumer protection lawyer who handles FDCPA cases. Your attorney will make sure Covington Credit not only sent you a debt validation letter within the five-day legally mandated period, but also that the company included the information required by the FDCPA.

Schedule a free initial consultation with an FDCPA lawyer to determine how to proceed with a case against Covington Credit.

Additional Resources

*Disclaimer: The content of this article serves only to provide information and should not be construed as legal advice. If you file a claim against Covington Credit, or any other third-party collection agency, you may not be entitled to compensation.