You are sitting comfortably on the couch in the living room reading one of your favorite books when the front doorbell rings. Startled, you slowly open the door to see someone dressed in a sharp looking suit holding a clipboard.

You are standing in front of a member of the judicial system who is about to serve you with a complaint summoning you to appear in court.

What to do if Global Credit & Collection sues you is more about acting with a sense of urgency than anything else. If you fail to respond to a lawsuit filed by the debt collection agency, the judge overseeing your case can issue a judgment against you to cover the cost of your debt, as well as court costs and attorney fees.

Not paying the money demanded within a judgment can force the court to garnish your wages, establish a lien on your property, and/or freeze all of your bank accounts. Once issued, a court ordered judgment cannot be revoked or modified in any way. You have to abide the stringent terms presented in the legal document.

Responding to a Complaint Filed by Global Credit & Collection

Despite the stress you feel after receiving a complaint from Global Credit & Collection, you have to act with a sense of urgency by speaking with a licensed consumer protection who specializes in litigating cases involving the Fair Debt Collection Practices Act (FDCPA).

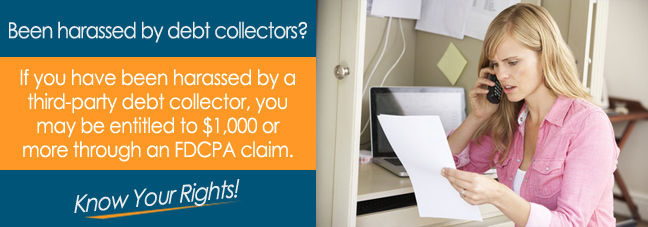

After decades of debt collection agency abuses, the FDCPA makes it illegal for a third party debt collector such as Global Credit & Collection to use overly aggressive debt collection tactics. For example, the groundbreaking federal consumer protection law prohibits bill collectors from calling consumers between 9 pm and 8 am.

The FDCPA also gives consumers the right to file claims against debt collection agencies. Your FDCPA attorney will thoroughly review your case to determine if there is enough evidence that Global Credit & Collection has violated one or more provisions of the FDCPA.

If there is not enough evidence, your lawyer can pursue other legally acceptable options, including asking a third party debt collector to negotiate in good faith to settle your outstanding credit card or your personal loan balance. Negotiating the settlement of a delinquent debt requires the skills of an experienced FDCPA lawyer who knows how to get you a deal you can afford, as well as a deal you can pay in a timely manner.

![What to Do If Global Credit & Collection Sues You*]()

Eligibility for Monetary Damages

The primary criterion for receiving monetary damages in a FDCPA case is to present evidence that proves a bill collector violated the consumer protection law. Having to deal with a debt collection agency can cause considerable stress, which can trigger one or more physical distress symptoms. With enough medical documentation and the testimony of healthcare professionals, you might be able to link the illegal actions of a third party debt collector to your physical ailments. Some of the symptoms of physical duress are skin rashes and long lasting ulcers.

Waiting out a bill collector when it comes to a lawsuit is not an option. You must be proactive by scheduling a free initial consultation with an accomplished consumer protection attorney who has compiled an impressive record litigating FDCPA cases.

Additional Resources

*Disclaimer: The content of this article serves only to provide information and should not be constructed as legal advice. If you file a claim against Global Credit & Collection or any other third-party collection agency, you may not be entitled to any compensation.