Passed by the United States Congress in September of 1977, the Fair Debt Collection Practices Act (FDCPA) leveled the playing field between consumers and third party debt collectors. The FDCPA clearly forbids debt collectors from making threats and using abusive language in attempts to collect delinquent consumer debts.

Third party debt collectors also must refrain from implementing deceptive debt collection tactics, such as impersonating law enforcement agencies. In response to the legal voids left by the FDCPA, states like California took the lead in establishing wage garnishment and statute of limitations guidelines.

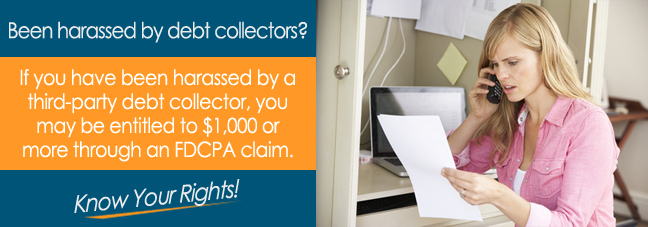

If National Commercial Services violates California law and/or the FDCPA, you have the right to speak with a licensed consumer protection law attorney.

What is the Statute of Limitations for Debt Collection?

The California Fair Debt Collection Practices Act (CFDCPA) defines how long third party debt collectors have to pursue collection of outstanding debts. As one of the shortest statute of limitations, debt collectors have four years to collect consumer debts created by written contracts.

Third party debt collectors have two years to collect debts formed by oral contracts. California law defines the starting date for the statute of limitations on the day when a debt collector wins a judgment in court to collect a delinquent consumer debt.

Can Debt Collectors Charge Fees and Interest?

Third party debt collectors make money by purchasing debts from original creditors for pennies on the dollar. In addition, many debt collectors like to charge additional fees and interest.

In California, debt collectors have the right to charge addition fees and interest, but only if the original contract contains language that permits the charging of additional fees and interest.

A licensed California consumer protection law attorney can help you determine whether the contract you signed with the original creditor allows a third party debt collector to tack on fees and interest charges.

![Collection Laws Governing National Commercial Services in CA*]()

California Wage Garnishment Law

In California, a third party debt collector must win a judgment in court to garnish your wages. If a third party debt collector threatens to garnish your wages, you should speak with an attorney to determine whether you have a case under the FDCPA to file a claim.

California law permits debt collectors to garnish wages by following a formula that is the lesser amount between 25% of your disposable income and 40 times the federal minimum wage.

An Experienced Consumer Law Attorney Can Help You

If left unchecked, many third party debt collectors resort to underhanded debt collection tactics. Your most effective counter attack is to speak with a FDCPA and CFDCPA attorney.

Your attorney will assist you in seeking the monetary damages you deserve for debt collector violations of state and federal law. Under the FDCPA statutory damages have a cap of $1,000. However, federal law does not limit the amount of money consumers can win for actual damages.

Additional Resources

*Disclaimer: The content of this article serves only to provide information and should not be constructed as legal advice. If you file a claim against National Commercial Services or any other third-party collection agency, you may not be entitled to any compensation.