American consumers are protected by several federal laws that ban unethical business practices. There are federal laws on the books that outlaw predatory lending policies, as well as give consumers the right to sue manufacturers for product defects.

Unfortunately, far too many consumers are unaware that they do not have to tolerate the aggressive tactics implemented by debt collection agencies.

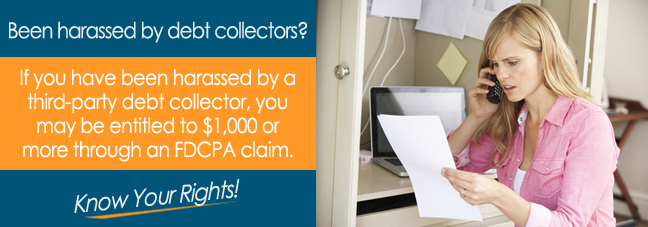

In response to consumer complaints, the United States Congress passed the Fair Debt Collection Practices Act on September 20, 1977. The monumental consumer protection law makes it illegal for third party debt collectors to harass consumers into paying off outstanding credit card and personal loan accounts.

Congress also added punitive provisions in the FDCPA, such as allowing consumers to file civil lawsuits against bill collectors to seek monetary damages for enduring pain and suffering.

Frequently Cited FDCPA Violations

Despite dozens of provisions written into the FDCPA that prohibit certain debt collection agency tactics, there are a few bad habits used by third party debt collectors that are the most frequently cited violations of the landmark consumer protection law.

For example, bill collectors like to use the telephone as a weapon to coerce consumers into paying off delinquent credit card and personal loan balances. The FDCPA forbids debt collection agencies from calling consumers between the hours of 9 pm and 8 am.

If a third party debt collector harasses you by repeatedly calling you at home or on your cell phone after 9 pm, you should immediately get in touch with a licensed consumer protection lawyer who specializes in litigating FDCPA cases.

Your FDCPA attorney will ask you several questions to ascertain whether National Service Bureau, Inc. harassed you by using abusive language or issuing direct threats.

Common harassment tactics used by bill collectors include threatening to size consumer property and threatening to contact close friends and family members in attempts to shame consumers into settling outstanding debts.

Debt collection agencies are not allowed to deceive consumers, such as impersonating a law enforcement agency and requesting more money that is actually owed on a delinquent debt.

![Starting a Claim Against National Service Bureau, Inc.*]()

Are You Eligible for Monetary Damages?

The FDCPA makes it clear that third party debt collectors can be on the financial hook for violating one or more provisions of the federal consumer protection law. You have the right to seek monetary damages for suffering from physical and/or emotional distress.

Emotional distress is much more difficult to prove, as it often entails analyzing the testimony of eyewitnesses and mental health professionals that can confirm the presence of symptoms.

The FDCPA also permits you to seek a one-time award up to $1,000 for statutory damages, which will punish a bill collector for violating the FDCPA. Your FDCPA lawyer will ask you if National Service Bureau, Inc. garnished any of your wages. Under the FDCPA, you have the right to recover every penny garnished by a law breaking bill collector.

Speak with an experienced consumer protection attorney today to learn how the FDCPA protects you against unlawful debt collection agency practices.

Additional Resources

*Disclaimer: The content of this article serves only to provide information and should not be constructed as legal advice. If you file a claim against National Service Bureau, Inc. or any other third-party collection agency, you may not be entitled to any compensation.