Because you received a phone call from Penn Credit, do you jump out of your seat every time your home and/or cell phone rings? Facing a relentless debt collector can send the most determined consumers into panic mode.

The physical and emotional distress caused by repeated debt collection agency phone calls spills over into every facet of your personal and professional lives. Stress morphs into acute anxiety, which makes you vulnerable to agreeing on the unfavorable debt settlement terms proposed by a third party debt collector.

If Penn Credit makes frequent phone calls to your home and/or cell phone, you can demand the bill collector stop making the phone calls. However, a powerful federal consumer protection law passed in 1977 does not include a provision that limits the number of phone calls debt collection agencies are permitted to make.

A debt collection agency such as Penn Credit can call you as much as it likes, but if the third party debt collector crosses the legal line, you have ways to make the phone calls stop.

Methods to Get Penn Credit to Stop Calling You

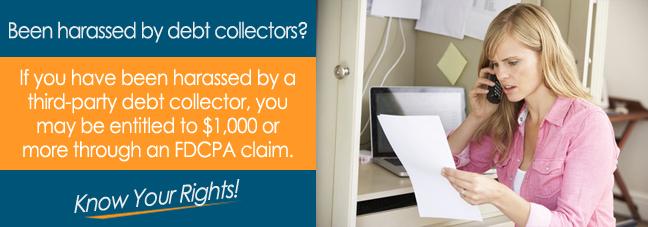

Trying to stop a bill collector from calling you can cause considerable stress. The first step on the road to eliminating debt collection agency phone calls involves knowing your rights under the Fair Debt Collection Practices Act (FDCPA).

Passed in 1977 by the United States Congress, the FDCPA offers consumers numerous legal protections to fight back against unethical third party debt collectors.

Instead of refusing to answer the phone or sending cell phone calls straight to voicemail, you should hired a licensed consumer protection lawyer to devise a strategy to stop Penn Credit phone calls.

Your FDCPA lawyer will help you draft a letter stating the tactics used by a bill collector to pursue an outstanding credit card or personal loan debt are illegal. Some of the tactics outlawed by the FPDCA include using abusive language and implementing deceptive debt collection techniques.

The letter you send Penn Credit should end with legal language that insists your FDCPA attorney will contact the Federal Trade Commission (FTC) and your state Attorney General Office if Penn Credit fails to cease using illegal debt collection practices.

![Debt Settlement Letter to Penn Credit*]()

Does the FDCPA Grant Consumers the Right to Seek Monetary Damages?

Let’s assume a debt collection agency has violated one or more provisions of the FDCPA. Do you have the right to sue the third party debt collector and seek monetary damages for the pain and suffering you experience.

The FDCPA allows consumers to fight back in court by seeking monetary damages for the physical and emotional distress caused by repeated phone calls. You also have the right to seek monetary damages for lost wages.

You might have called off sick several times or your employer scheduled you less because of a loss in productivity. Your consumer protection lawyer will need to obtain time records to validate your legal claim.

If you had wages garnished as mandated by a bill collector initiated legal action, you have the right to have the wages returned to your bank account because of one or more FDCPA violations.

Do not allow a debt collection agency to push you around by making frequent phone calls. Speak with an experienced FDCPA lawyer today to learn more about how the landmark federal law protects consumers against unethical third party debt collectors.

Additional Resources

*Disclaimer: The content of this article serves only to provide information and should not be constructed as legal advice. If you file a claim against Penn Credit or any other third-party collection agency, you may not be entitled to any compensation.